The Automated ICS: Future Tools for Instant Incurred Cost Filing

The incurred cost submission deadline doesn’t move. But for most small contractors, the preparation process still looks like it did twenty years ago.

I’ve sat with contractors in the final weeks before their incurred cost submission was due — spreadsheets open across three monitors, a stack of reconciliation notes from the prior year serving as the only documentation of how the schedule was built, and a CFO who hadn’t slept properly in two weeks. The submission got filed. It was late. It was incomplete on two schedules. DCAA issued a determination of inadequacy, the clock reset, and the whole process started over — this time with an auditor actively involved in the reconstruction.

That scenario isn’t unusual. For small and mid-size government contractors, the incurred cost submission is the single most labor-intensive annual compliance obligation they face. And the tools most firms are using to meet it — disconnected spreadsheets, manual rate calculations, and year-end data pulls from accounting systems not designed for the purpose — are the reason it stays that way.

That is changing. Automated incurred cost submission tools are moving from enterprise-only solutions to accessible platforms for contractors of any size. Understanding what those tools need to do — and what the regulations require — is the starting point for building a submission process that doesn’t consume your organization every spring.

The Legal Foundation

The incurred cost submission requirement is not optional, and it is not a form that can be approximated. The regulatory framework is specific about what must be filed, when, and to what standard of adequacy.

FAR 52.216-7, the Allowable Cost and Payment clause, is the contractual authority for the incurred cost submission requirement. It requires contractors performing cost-reimbursement contracts to submit a final indirect cost rate proposal — the incurred cost submission — within six months of the close of each fiscal year. The submission must include all schedules specified in the clause and must be adequate for audit. If DCAA determines the submission is inadequate, the contractor must refile, and the six-month adequacy clock restarts from the date of the revised submission.

FAR 31.201-2 establishes that costs charged to government contracts must be allowable, allocable, reasonable, and consistently treated. The incurred cost submission is the annual mechanism through which contractors demonstrate that every cost charged during the year met those four tests. An automated system that continuously monitors cost transactions against these standards — flagging unallowable costs, verifying allocability, and tracking consistency with disclosed practices — transforms the submission from a year-end reconstruction into a continuous compliance record.

For contractors subject to Cost Accounting Standards, CAS 401 requires that cost accounting practices used in accumulating and reporting costs be consistent with the practices used in estimating. The incurred cost submission is where that consistency is tested annually. If your actual cost accumulation practices drifted from your disclosed methodology during the year, the submission is where that drift becomes visible — and where the exposure materializes. The DCAA Incurred Cost Electronically submission guidance outlines the current ICE model requirements and is the most practical reference available for understanding what an adequate submission contains.

Why Manual Processes Break Down

Here’s what contractors miss: the incurred cost submission isn’t difficult because the math is complex. It’s difficult because the underlying data — labor costs by contract, indirect costs by pool, direct versus indirect classifications, unallowable cost identification — must be organized consistently throughout the year in order to be assembled accurately at year-end. When it isn’t, the submission process becomes a forensic exercise rather than a reporting exercise.

The first failure point is unallowable cost identification. FAR 31.2 identifies specific cost categories that cannot be charged to government contracts — entertainment, certain lobbying costs, unallowable compensation elements, and others. These costs must be identified and excluded from indirect cost pools before rates are calculated. Contractors using manual processes often handle this through year-end adjustments — a journal entry that moves unallowable costs out of the pool after the fact. This is where audits go sideways. Unallowable costs that flowed through the pool during the year, even temporarily, can affect provisional billing rates and create questions about whether those costs influenced interim billings.

The second failure point is indirect rate reconciliation. The incurred cost submission requires contractors to reconcile their final indirect rates to their provisional billing rates and explain any variance. When provisional rates were set at the beginning of the year using estimates, and actual costs diverged significantly from those estimates, the reconciliation can be complex. Manual systems that didn’t track rate-sensitive costs in real time make this reconciliation a retrospective puzzle rather than a documented progression.

The third failure point is schedule completeness. DCAA’s adequacy checklist for the incurred cost submission covers more than a dozen schedules — direct costs by contract, indirect cost pool statements, rate calculations, subcontractor information, and more. Submissions that are missing schedules, or that contain schedules with internal inconsistencies, are returned as inadequate regardless of how accurate the underlying numbers are. A manual process dependent on one person’s institutional knowledge of which schedules are required and how they connect is fragile by design.

What Automated ICS Tools Are Starting to Do

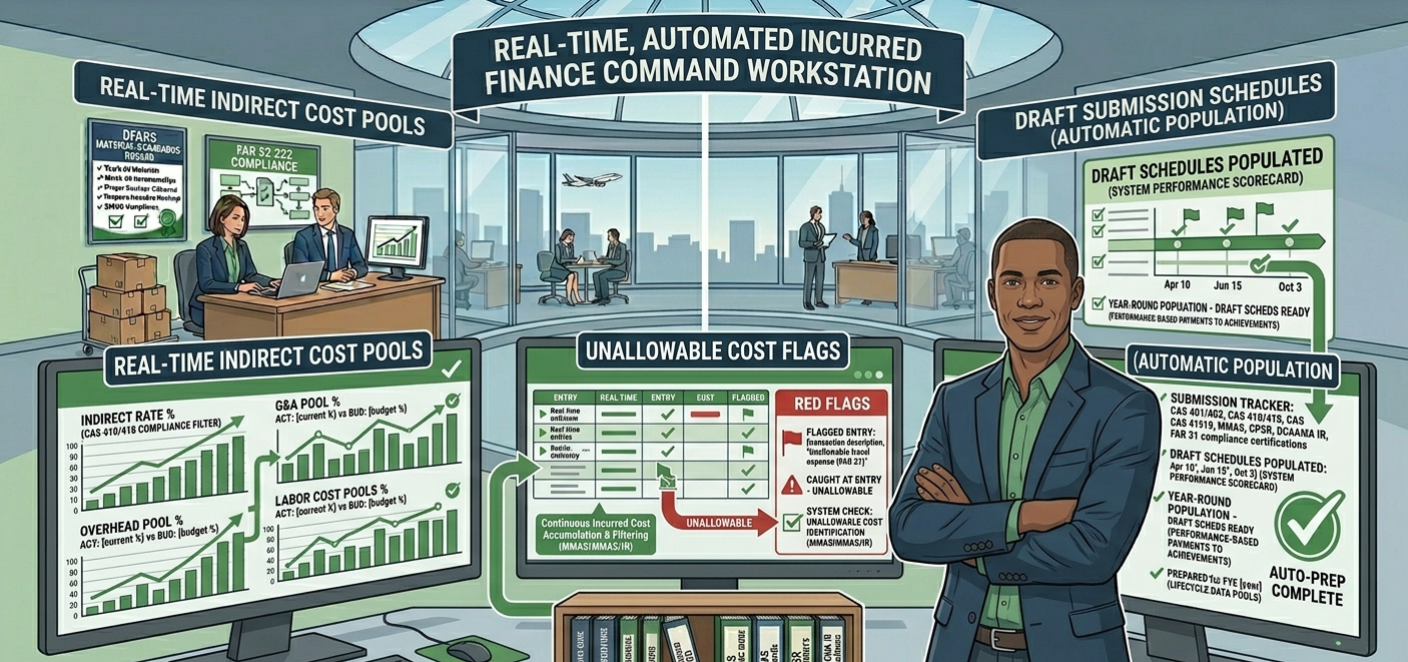

The most significant shift in incurred cost submission technology is the move from year-end assembly to continuous accumulation. Emerging automated tools — and the next generation of DCAA-compliant accounting platforms — are designed to maintain submission-ready data throughout the fiscal year rather than requiring a year-end data extraction and reorganization.

The core capabilities that matter for a small contractor are straightforward. The system should flag transactions that may contain unallowable costs at the time of posting — not at year-end. It should maintain running indirect cost pool balances by pool category in the same structure used for rate calculations. It should track direct costs by contract in a format that maps directly to the submission schedules. And it should produce draft submission schedules on demand, so that the year-end process is a review and certification rather than a construction project.

The labor charging foundation is particularly important. Because labor is the largest cost element for most service contractors and the primary driver of indirect rate calculations, a DCAA-compliant timekeeping system that feeds accurate, contract-coded labor data directly into the cost accumulation structure is the most impactful single investment a contractor can make toward submission automation. Labor data that flows cleanly from timesheet to job cost ledger to indirect rate calculation eliminates the most error-prone manual step in the entire process.

Five Steps to Modernize Your ICS Process

Step 1: Map your current submission process to identify where manual intervention occurs. Walk through last year’s submission preparation and document every point where data was manually extracted, reformatted, or adjusted. Each of those points is a potential automation target — and a current source of error risk. The goal is to understand your baseline before selecting tools to improve it.

Step 2: Align your chart of accounts to the ICS schedule structure. The incurred cost submission schedules have a defined structure. Your general ledger should mirror that structure so that schedule population is a direct export rather than a manual mapping exercise. If your accounting system uses cost categories or pool definitions that don’t align with the submission format, this is the year to fix it. For guidance on structuring your cost accounting for compliance, see our post on incurred cost submission preparation.

Step 3: Implement continuous unallowable cost identification. Work with your accounting team to establish a standard set of general ledger accounts — or account flags — for cost categories with unallowable exposure: entertainment, certain travel, executive compensation above thresholds, and others. When these costs are identified at posting rather than at year-end, the submission process becomes a verification exercise rather than a discovery process.

Step 4: Establish a quarterly ICS pre-check process. Treat the incurred cost submission as a quarterly deliverable rather than an annual one. Every quarter, pull draft versions of your key submission schedules — indirect cost pool statements, rate calculations, direct cost summaries — and reconcile them to your general ledger. Quarterly pre-checks catch discrepancies while they’re still manageable and eliminate the year-end crisis that manual processes inevitably produce.

Step 5: Evaluate submission-ready accounting platforms before your next fiscal year begins. The market for DCAA-compliant accounting tools with integrated ICS functionality is expanding. When evaluating platforms, the key criteria are: does it maintain indirect cost pools in real time, does it flag unallowable cost categories at transaction entry, does it produce draft submission schedules in the ICE model format, and does it integrate with your timekeeping system without manual data transfer? A platform that meets all four criteria eliminates the majority of the manual labor in your current process. Hour Timesheet’s integration with DCAA-compliant accounting systems is designed specifically to support this kind of automated cost accumulation.

The Cost Comparison

An incurred cost submission prepared manually — data extraction, schedule construction, reconciliation, review, and filing — typically consumes between 80 and 200 hours of internal staff time annually for a small contractor, plus outside CPA or consultant fees that commonly run between $5,000 and $20,000 depending on contract complexity.

An inadequacy determination from DCAA resets that clock entirely. The contractor must refile, DCAA must re-review, and the audit cycle extends — sometimes by years. Contractors with multiple years of open incurred cost audits face compounding exposure: provisional billing rates that may need retroactive adjustment, potential refund obligations on overbilled costs, and audit costs that accumulate with each open year.

Automated tools that reduce submission preparation time by half — a conservative estimate for systems with real-time pool tracking and schedule generation — pay for themselves in staff time savings alone within the first year. The reduction in adequacy risk, audit exposure, and outside consultant fees makes the return substantially higher.

Jurisdictional Notes

The incurred cost submission requirement under FAR 52.216-7 applies to all cost-reimbursement contracts across both DoD and civilian federal agencies. DCAA has audit jurisdiction primarily over DoD contracts, but civilian agency audit organizations — including agency Inspectors General and the GSA OIG — conduct incurred cost audits under the same FAR framework. Contractors with mixed portfolios spanning DoD and civilian agencies should build their submission process to satisfy both audit environments, which the FAR-based ICE model format accomplishes by design.

The incurred cost submission will always require professional judgment and careful review. What automation removes is the annual scramble — the manual data pulls, the schedule reconstruction, the last-minute reconciliation. Build your accounting infrastructure to accumulate submission-ready data continuously, and the submission itself becomes what it was always supposed to be: a straightforward annual report on costs you already understand.

Hour Timesheet gives government contractors the timekeeping foundation that makes automated incurred cost submission possible — clean, contract-coded labor data flowing directly into your cost accumulation system all year long. Learn how our platform supports your ICS process.