Subcontractor Oversight: Monitoring Financial Health for DCAA Compliance

Your company awarded a $4.2 million critical path subcontract to a vendor whose financial statements showed strong revenues and growth—but during contract execution, the subcontractor declared bankruptcy, defaulted on deliverables, and left you scrambling to find replacement sources while absorbing $680,000 in reprocurement costs that DCAA questioned as avoidable contractor mismanagement because you failed to monitor the subcontractor’s deteriorating financial condition despite warning signs including delayed invoicing, payment disputes with other customers, and declining credit ratings. Here’s what contractors miss about subcontractor financial oversight: your responsibility doesn’t end at subcontract award—you must actively monitor subcontractor financial health throughout performance identifying indicators of financial distress requiring intervention, mitigation planning, or alternative sourcing before problems escalate into performance failures creating cost impacts, schedule delays, or quality issues that prime contract responsibility ultimately charges to your account regardless of whether subcontractor caused underlying problems. Understanding how to assess, monitor, and respond to subcontractor financial risks isn’t about becoming their banker—it’s about protecting contract performance through early identification of financial warning signs enabling proactive management preventing the catastrophic failures that inadequate financial oversight allows to develop undetected until remediation becomes impossible and contract consequences become inevitable.

The Legal Framework Governing Subcontractor Financial Oversight

Federal acquisition regulations establish prime contractor responsibility for ensuring subcontractor capability and managing subcontractor performance protecting government interests. FAR 44.202-2 requires contractors to assess prospective subcontractors’ responsibility including financial capability before award, evaluating whether subcontractors possess adequate financial resources to perform or the ability to obtain them. This pre-award assessment creates baseline obligation, but ongoing financial monitoring extends this responsibility throughout contract performance ensuring capabilities verified at award continue supporting successful delivery.

The subcontractor surveillance requirements under DFARS 252.244-7001(c)(16) mandate that purchasing systems include procedures for evaluating subcontractor performance, which encompasses both technical delivery and business capability including financial stability affecting performance reliability. Understanding DCAA compliance requirements means recognizing that subcontractor management represents ongoing responsibility requiring systematic monitoring rather than one-time verification at source selection, with financial health monitoring essential to detecting emerging risks before they compromise contract outcomes.

The cost allowability implications under FAR 31.201-2 establish that costs must result from prudent business judgment and sound business practices, meaning reprocurement costs resulting from preventable subcontractor failures due to inadequate financial monitoring may be questioned as imprudent contractor management rather than allowable contract costs. When financial distress indicators were observable through reasonable due diligence but contractors failed to identify or address them, resulting failure costs represent contractor mismanagement rather than unforeseeable business risks, creating questioned cost exposure when DCAA examines circumstances surrounding subcontractor defaults and prime contractor oversight adequacy.

The critical consideration involves FAR 42.1502, governing contractor business systems including purchasing systems that must ensure effective subcontract management. Financial monitoring represents key element of effective management, with systematic procedures ensuring that financial risks receive ongoing assessment rather than remaining invisible until manifested through performance failures requiring costly remediation or replacement sourcing under unfavorable circumstances.

What Contractors Must Understand About Subcontractor Financial Monitoring Challenges

Here’s what contractors miss about financial oversight: subcontractors experiencing financial difficulties rarely volunteer problems until situations become critical—you need proactive monitoring detecting warning signs through financial statement analysis, payment pattern observation, and market intelligence gathering rather than relying on subcontractor disclosure of problems they’re incentivized to conceal. DCAA compliance explained emphasizes that due diligence requires active investigation not passive receipt of whatever information vendors choose to provide, with contractors bearing responsibility for identifying risks through reasonable inquiry even when subcontractors attempt concealment.

The pre-award assessment gap emerges when contractors conduct superficial financial reviews at source selection—reviewing D&B reports or requesting financial statements—without rigorous analysis evaluating financial strength, liquidity, leverage, profitability trends, or cash flow adequacy supporting proposed work. This is where audits go sideways—your procurement team selected the low bidder after confirming they were “financially viable” through cursory review, but deeper analysis would have revealed declining margins, increasing debt, negative cash flow, and deteriorating working capital indicating financial stress making contract performance risky. Without analytical rigor at award, you’ve missed the baseline assessment that ongoing monitoring requires for comparison detecting deterioration.

The ongoing monitoring void surfaces when contractors lack systematic procedures requiring periodic financial statement review, payment performance monitoring, or financial health reassessment throughout contract performance. Most contractors review financial capability once at award then never again unless obvious problems emerge—by which time intervention options have narrowed and damage mitigation becomes reactive crisis management rather than proactive risk mitigation. DCAA timekeeping requirements extend conceptually to subcontractor management requiring documented evidence of ongoing oversight demonstrating continuous attention to performance risks including financial capability maintenance.

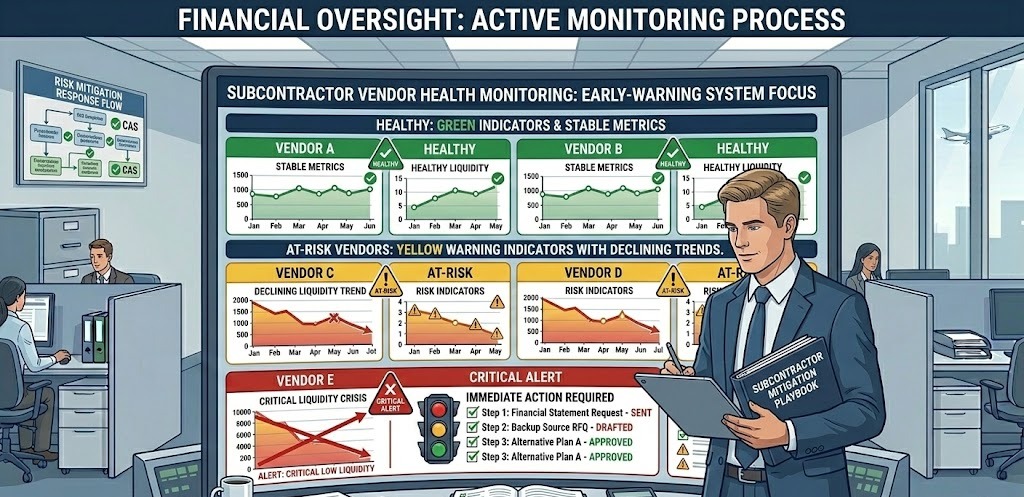

The warning sign recognition failure appears when contractors observe concerning indicators but don’t recognize their significance or investigate underlying causes including: delayed invoice submission suggesting cash flow problems, frequent payment term extension requests indicating liquidity constraints, increased billing disputes potentially masking financial desperation, personnel turnover especially in key management or technical positions, facility or equipment deterioration reflecting investment cutbacks, or slow payment to their own suppliers creating supply chain vulnerabilities. These observable signs signal financial distress requiring investigation and mitigation planning, but contractors lacking financial monitoring awareness miss their significance until accumulating problems trigger catastrophic failure.

The relationship management tension creates challenges when financial monitoring appears adversarial to subcontractor relationships—contractors hesitate requesting financial updates or investigating concerning signs fearing vendor reactions or relationship damage. However, prudent business management requires understanding counterparty financial health, with professional subcontractors recognizing legitimate oversight interest while problem vendors resisting transparency revealing distress they prefer concealing. Relationship concerns cannot override fiduciary responsibility for performance protection, requiring contractors to balance courtesy with necessary due diligence ensuring subcontractor capability throughout performance.

The mitigation planning inadequacy manifests when contractors identify financial concerns but lack response procedures including: increasing surveillance of deliverables and quality, requiring advanced deliveries or performance demonstrations, obtaining performance bonds or other security, developing backup source relationships, or creating transition plans enabling rapid replacement sourcing if problems escalate. Early warning detection provides value only when coupled with response planning converting intelligence into action preventing or mitigating failures before they compromise contract outcomes.

The cost impact documentation gap emerges when subcontractor financial failures create reprocurement costs but contractors lack documentation demonstrating that reasonable financial oversight occurred and that failures resulted from unforeseeable circumstances rather than inadequate monitoring. Without contemporaneous documentation showing financial assessment at award and periodic monitoring during performance, DCAA cannot verify that prudent business practices were followed, creating questioned cost vulnerability when expensive failures occur from what auditors may view as preventable contractor mismanagement.

Five Essential Steps for Effective Subcontractor Financial Monitoring

Step 1: Conduct Rigorous Pre-Award Financial Capability Assessment

Implement comprehensive pre-award financial analysis procedures for significant subcontracts requiring: financial statement collection (typically three years), ratio analysis evaluating liquidity, profitability, leverage, and efficiency, trend analysis identifying improving or deteriorating financial performance, cash flow adequacy assessment evaluating ability to fund proposed work, and working capital analysis determining resources available for contract execution. Create standardized financial assessment templates ensuring consistent rigorous evaluation rather than cursory reviews providing false assurance about financial capability.

Establish financial assessment thresholds triggering enhanced due diligence for higher-risk or higher-value subcontracts, with sophisticated analysis for critical or large procurements while simplified reviews suffice for routine commodity purchases from established suppliers. Scalable procedures focus resources where financial risk warrants intensive evaluation while maintaining efficiency for low-risk procurements.

Develop financial assessment documentation requirements capturing analysis performed, concerns identified, risk mitigation approaches, and approval rationale when proceeding despite identified financial concerns. This contemporaneous record establishes baseline financial condition for future comparison while documenting that award decisions reflected informed risk acceptance rather than uninformed negligence when problems subsequently emerge.

Step 2: Establish Systematic Ongoing Financial Monitoring Procedures

Deploy periodic financial review requirements for active subcontracts based on contract value, criticality, and initial financial assessment, with higher-risk relationships receiving more frequent monitoring (quarterly or semi-annually) while stable low-risk vendors undergo annual review. Request updated financial statements, review credit reports for rating changes, monitor payment performance for patterns suggesting cash flow problems, and conduct relationship reviews with subcontractor personnel identifying business condition changes affecting performance capability.

Implement early warning indicator monitoring including: invoice submission timing and patterns, payment term modification requests, billing dispute frequency, personnel turnover rates especially in leadership, facility condition observations, supply chain payment rumors or complaints, and market intelligence about business challenges, ownership changes, or strategic shifts. Systematic indicator tracking identifies concerning trends requiring investigation before isolated incidents accumulate into crisis patterns.

Create monitoring documentation requirements recording financial reviews conducted, findings identified, actions taken addressing concerns, and ongoing risk assessments evaluating whether relationships remain acceptable or require mitigation planning. Documentation demonstrates ongoing oversight discharging due diligence responsibilities while providing evidence supporting that financial monitoring occurred when DCAA examines circumstances surrounding any subsequent problems.

Step 3: Develop Financial Analysis Capability and Decision Criteria

Train procurement and program management personnel in basic financial statement interpretation, ratio calculation and analysis, trend identification, and warning sign recognition, enabling staff to conduct meaningful financial reviews rather than perfunctory document collection. Financial literacy transforms monitoring from compliance checkbox into risk management tool providing genuine business intelligence supporting procurement decisions.

Establish financial health criteria defining acceptable standards including: minimum current ratio or working capital levels, maximum debt-to-equity ratios, minimum profitability margins, positive cash flow requirements, or credit rating minimums for different contract types and risk levels. Objective criteria provide decision frameworks for evaluating whether financial conditions support contract award or continuation, reducing subjective judgment while enabling consistent risk-based procurement decisions.

Deploy analytical tools or templates automating ratio calculations, trend analysis, and comparison to established standards, enabling efficient financial assessment by procurement personnel without requiring specialized accounting expertise for routine analysis while flagging situations requiring expert consultation. Technology leverage makes sophisticated financial monitoring practical for organizations lacking dedicated financial analysis staff.

Step 4: Implement Risk Mitigation and Response Procedures

Create tiered response procedures triggered by financial concern severity including: increased surveillance and monitoring for minor concerns, performance security requirements (bonds, guarantees, escrow) for moderate risks, accelerated delivery or demonstration requirements for significant worries, backup source development for high risks, and transition planning for critical threats. Graduated responses enable proportional reactions matching mitigation intensity to risk magnitude.

Establish cross-functional risk assessment teams for significant financial concerns bringing together procurement, program management, quality, and finance personnel evaluating situation severity, performance impact potential, and appropriate mitigation approaches. Collaborative assessment leverages diverse perspectives preventing narrow procurement or program views missing important risk dimensions while building organizational consensus supporting mitigation decisions.

Develop transition and replacement sourcing procedures enabling rapid response when financial distress escalates requiring subcontractor replacement, including: alternative source identification and qualification, transition planning minimizing performance gaps, cost impact assessment and customer notification, and documentation supporting reprocurement cost allowability through evidence that reasonable mitigation occurred before situations became irreparable.

Step 5: Maintain Comprehensive Financial Oversight Documentation

Create subcontractor management files consolidating: pre-award financial assessments and approval documentation, periodic financial review records and analysis, early warning indicator logs tracking concerning observations, risk mitigation plans and implementation evidence, and correspondence with subcontractors about financial concerns or performance implications. Organized files support both operational decision-making and retrospective verification demonstrating oversight adequacy when failures occur despite reasonable monitoring.

Implement financial monitoring reporting providing management visibility into subcontractor portfolio financial health including: aggregate risk assessments, individual high-risk relationships requiring attention, early warning trends affecting multiple vendors, and recommended actions addressing identified concerns. Management reporting ensures financial risks receive appropriate attention while enabling executive oversight of subcontractor management effectiveness.

Document lessons learned from subcontractor financial problems including: how warning signs manifested, whether monitoring procedures detected them promptly, what response actions proved effective or ineffective, and what procedural improvements would enhance future monitoring. Systematic learning converts problems into organizational capability improvements strengthening financial oversight and risk management across subcontractor portfolio.

The Investment in Subcontractor Financial Monitoring Excellence

Implementing comprehensive subcontractor financial monitoring costs between $15,000 and $45,000 for small to mid-sized contractors including procedure development, training delivery, analytical tool deployment, and initial assessment conduct. Annual maintenance costs typically run $8,000 to $25,000 for ongoing monitoring, periodic assessments, and program management depending on subcontractor portfolio size and complexity.

Let me show you the value: contractors with effective financial monitoring identify risks early enabling proactive mitigation preventing catastrophic failures and expensive reprocurement costs. They demonstrate prudent business management through documented oversight supporting cost allowability when despite best efforts some failures prove unavoidable. They maintain better subcontractor relationships through professional engagement demonstrating serious business partnership rather than casual vendor management.

Contractors with inadequate financial monitoring face substantial questioned costs when preventable subcontractor failures create expensive remediation that auditors attribute to contractor mismanagement rather than unforeseeable business risks. They experience contract performance problems from financial failures that reasonable oversight would have detected enabling mitigation or alternative sourcing. They suffer reputation damage when subcontractor problems compromise prime contract delivery suggesting inadequate procurement management.

Understanding Financial Oversight Requirements Across Contract Types

Subcontractor financial oversight requirements apply most explicitly to cost-reimbursement contracts where reprocurement costs directly affect government reimbursement, but prudent business practice extends monitoring to all contract types where subcontractor failures impact performance regardless of contract structure. Fixed-price primes face greater financial exposure from subcontractor problems but identical performance obligations requiring effective financial monitoring protecting delivery commitments.

FAR purchasing system requirements and prudent business practice standards apply uniformly across Department of Defense, NASA, Department of Energy, and civilian agency contracts, with financial monitoring representing universal best practice rather than agency-specific obligation. Your oversight procedures should satisfy requirements across all customers through comprehensive approach serving entire contract portfolio.

Your Path to Subcontractor Financial Oversight Success

The subcontractor financial monitoring landscape rewards contractors who invest in systematic assessment, ongoing surveillance, and proactive risk mitigation rather than reactive crisis response after problems become irreparable. DCAA evaluates subcontractor oversight through documentation review examining whether contractors exercised reasonable due diligence protecting government interests through prudent subcontractor management.

For contractors seeking financial monitoring capability, Hour Timesheet provides labor tracking documenting procurement and program management staff time spent on subcontractor oversight activities, demonstrating organizational investment in relationship management supporting system adequacy verification and cost allowability justification.

Your subcontractor relationships deserve systematic financial monitoring protecting contract performance through early risk identification and proactive mitigation. Implement procedures ensuring financial oversight throughout relationship lifecycle from pre-award assessment through performance completion.