Interest Penalties under the Prompt Payment Act: GovCon Guidelines

Your company submitted a proper invoice on June 15 for completed contract deliverables, but the government didn’t process payment until September 3—79 days later—triggering automatic interest penalties of $8,400 under the Prompt Payment Act that the government paid you without dispute. Six months later during your incurred cost audit, DCAA questioned whether you properly accounted for this interest income, discovering you had failed to credit it against contract costs or indirect rates as regulations require, creating $8,400 in questioned costs plus cascading impacts on indirect rate calculations affecting multiple contracts. Here’s what contractors miss about Prompt Payment Act interest: while the Act protects contractors from payment delays through automatic interest penalties, federal cost accounting rules require specific treatment of this interest income—you must credit it against the costs that generated the original invoices, offset indirect pool costs when interest relates to indirect cost billings, or credit G&A pools when interest stems from general billing, not treat interest as general business income disconnected from cost accounting impact. Understanding how to account for, allocate, and report Prompt Payment interest isn’t about maximizing retention of penalty payments—it’s about ensuring interest credits reduce costs charged to government contracts as cost principles require, maintaining proper accounting treatment distinguishing interest from operations income, and documenting methodology proving compliance with credit requirements that DCAA verifies through systematic review during incurred cost audits.

The Legal Framework Governing Prompt Payment Interest Treatment

The Prompt Payment Act establishes mandatory payment timelines and automatic interest penalties protecting contractors from government payment delays. 31 USC 3901-3907 requires federal agencies to pay contractors within specified periods after receiving proper invoices—typically 30 days—with automatic interest penalties accruing on late payments calculated using Treasury rates without requiring contractor requests or claims. This statutory protection ensures contractors don’t finance government operations through payment delays, providing compensation for cash flow impacts and opportunity costs that late payments create.

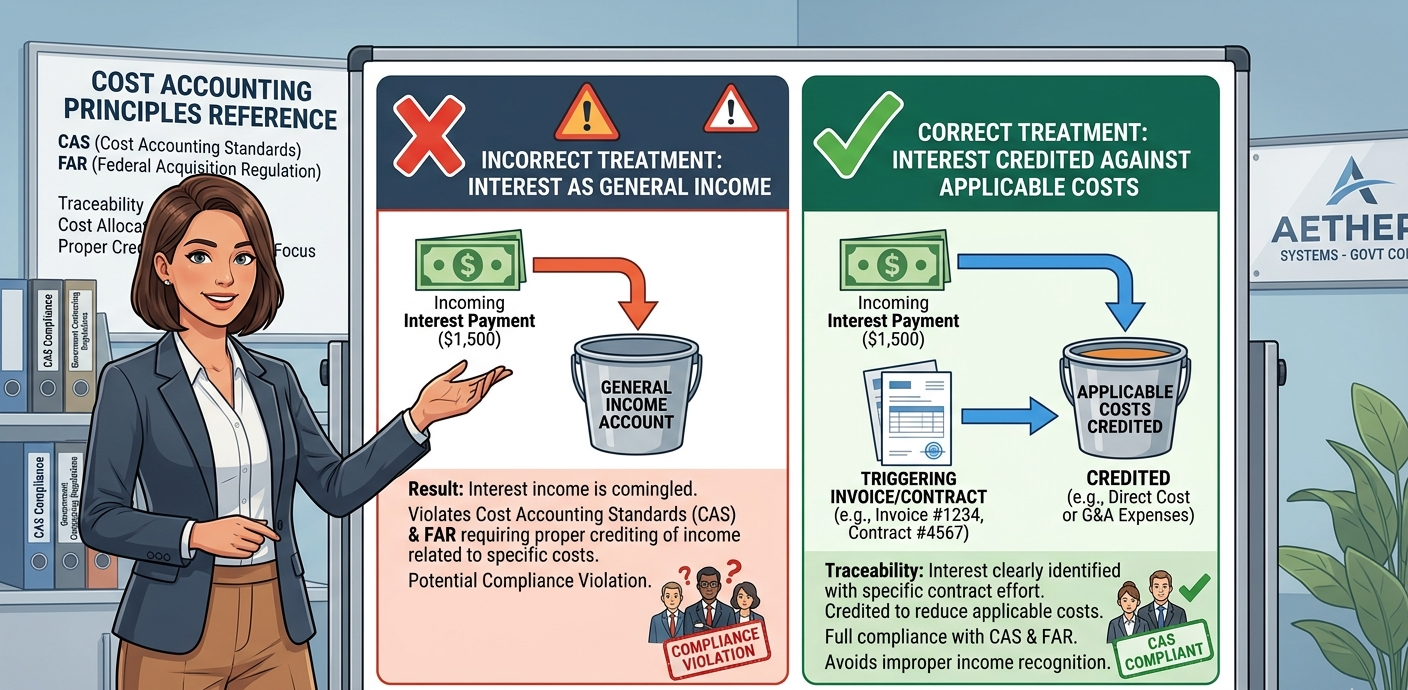

The cost accounting treatment requirements under FAR 31.205-17 establish that interest income must be credited against interest expense in the same cost period, with any excess interest income after offsetting interest expense credited to the cost objectives that generated the underlying payments triggering interest. Understanding DCAA compliance requirements means recognizing that Prompt Payment interest isn’t bonus income contractors retain—it’s compensation for late payment requiring specific accounting treatment reducing costs charged to government contracts through systematic crediting procedures DCAA verifies during audits.

The specific crediting methodology under FAR 31.201-5 governs credits, requiring amounts that benefit contracts or otherwise reduce costs charged to government work to be credited to cost objectives or indirect pools. For Prompt Payment interest, this means identifying which invoice generated interest, determining whether invoice charged direct costs to specific contracts or indirect costs to pools, and crediting interest appropriately—direct contract interest credits the specific contract, indirect cost interest credits the applicable indirect pool, and mixed invoice interest allocates proportionally across affected cost objectives.

The critical consideration involves FAR 52.232-25, the Prompt Payment clause included in government contracts establishing payment timelines, interest calculation methodologies, and contractor rights to automatic interest without filing claims when agencies miss payment deadlines. This clause makes interest a contractual right rather than discretionary payment, but doesn’t modify underlying cost accounting obligations requiring proper interest treatment in contractor accounting systems and government contract billing.

What Contractors Must Understand About Prompt Payment Interest Challenges

Here’s what contractors miss about interest accounting: receiving Prompt Payment interest feels like penalty income compensating for government administrative failures, tempting treatment as general business income rather than cost reductions requiring systematic crediting against contracts or indirect pools. DCAA compliance explained emphasizes that regulatory treatment depends on cost accounting principles rather than payment characterization, with interest representing cost offsets regardless of whether government or contractor caused underlying payment delays.

The accounting classification error emerges when contractors record Prompt Payment interest as miscellaneous income, other revenue, or financial income rather than as credits against cost pools or specific contracts. This is where audits go sideways—your accounting system posts interest to income statement revenue accounts increasing net income, but FAR requires crediting against costs reducing amounts charged to government contracts. When DCAA discovers interest treated as income rather than cost credits during incurred cost audits, questioned costs equal full interest amounts plus any indirect rate impacts from pool cost overstatements, potentially doubling the cost accounting error beyond simple interest misclassification.

The invoice tracing inadequacy surfaces when contractors receive Prompt Payment interest but cannot determine which original invoices generated the interest payments, preventing proper crediting to applicable contracts or cost pools. Government interest payments often arrive months after original invoices with payment descriptions lacking clear cross-references to triggering invoices, requiring contractors to maintain detailed accounts receivable tracking enabling retroactive matching between interest receipts and underlying invoices. DCAA timekeeping requirements extend conceptually to payment tracking requiring documentation supporting cost accounting treatment including invoice-to-interest matching enabling proper crediting.

The mixed invoice allocation challenge appears when single invoices combine direct costs from multiple contracts plus indirect cost billings, with resulting Prompt Payment interest requiring proportional allocation across all cost elements included in original invoice. Your monthly billing might invoice $200,000 direct costs for Contract A, $150,000 for Contract B, and $50,000 indirect cost billings, with $4,000 interest requiring allocation: $2,000 to Contract A (50%), $1,500 to Contract B (37.5%), and $500 to indirect pools (12.5%). Without this proportional treatment, interest credits don’t properly offset all affected cost objectives as regulations require.

The interest expense offset requirement creates accounting complications when contractors incur interest expense on business financing that must be offset by interest income before any excess credits against contracts or indirect pools. FAR 31.205-20 generally makes interest expense unallowable, but when contractors do incur interest expense (often unallowable), Prompt Payment interest must first offset this expense with only excess amounts credited to cost objectives. This sequencing affects credit amounts and requires documentation supporting offset calculations before determining contract or pool credits.

The indirect rate calculation impact appears when Prompt Payment interest relating to indirect cost billings should credit applicable pools reducing pool totals before rate calculations, but contractors fail to process credits timely, allowing overstated pool costs to inflate indirect rates affecting all contracts using those rates. When monthly overhead or G&A billings generate interest, monthly or quarterly crediting prevents rate distortion, while delayed annual crediting allows temporary rate inflation affecting interim billing and potentially requiring rate adjustments and customer reconciliation.

The timing and period matching consideration affects when interest credits impact costs, with FAR generally requiring costs and credits to affect the same accounting period. Prompt Payment interest accruing in one fiscal year but received in the next creates period matching questions requiring judgment about whether to adjust prior period costs through retroactive credit or treat current period receipts as current year credits. Documentation supporting timing decisions demonstrates reasoned methodology rather than arbitrary or opportunistic period selection affecting cost recovery patterns.

Five Essential Steps for Prompt Payment Interest Compliance

Step 1: Establish Systematic Interest Income Identification and Recording

Implement accounts receivable procedures requiring identification of all Prompt Payment interest receipts through payment description review, remittance advice examination, or government payment system data analysis. Configure accounting systems with dedicated interest income accounts separate from operational revenue, enabling clear interest tracking distinct from contract revenue while preventing inadvertent treatment as general business income bypassing cost crediting requirements.

Develop interest receipt documentation procedures requiring capture of payment dates, amounts, calculation details when provided by government, and most importantly, identification of underlying invoice triggering interest through payment reference analysis or accounts receivable aging review. Maintain detailed interest receipts logs showing for each interest payment: receipt date, amount, source agency, triggering invoice identification, and cost accounting treatment determination.

Deploy monthly reconciliation procedures comparing total interest income recorded to government payment records, investigating discrepancies suggesting missing interest receipts or recording errors, and validating that all identified interest receives proper accounting treatment. Systematic reconciliation prevents interest receipts from escaping cost crediting through recording gaps or classification errors.

Step 2: Develop Invoice Tracking Enabling Interest-to-Cost-Objective Matching

Create comprehensive invoice tracking systems maintaining detailed records for each customer invoice including: invoice number and date, contract identifications and amounts by contract, indirect cost billing amounts by pool type, total invoice amount, payment due date, actual payment date, and any Prompt Payment interest received. Organized tracking enables efficient matching between interest receipts and triggering invoices supporting proper cost crediting.

Implement accounts receivable aging procedures maintaining visibility into unpaid invoices approaching and exceeding Prompt Payment timelines, enabling both proactive collection follow-up and anticipation of likely interest accruals requiring future accounting treatment. Aging visibility supports cash management while enabling interest accrual estimates improving monthly financial reporting and cost accounting accuracy before actual interest receipts.

Establish invoice-interest matching procedures using payment dates, amounts, and descriptions to identify which invoices generated interest payments, documenting matches in both interest logs and invoice records creating bidirectional audit trail supporting cost crediting determinations. When matching proves uncertain due to inadequate government payment descriptions, document reasonable matching methodology based on payment timing, amount correlation, or other available evidence rather than abandoning crediting requirements due to documentation challenges.

Step 3: Implement Proper Interest Crediting Methodology and Documentation

Develop interest crediting procedures documenting how to credit different interest types including: direct contract interest credits the specific contract identified in triggering invoice, indirect pool interest credits applicable pool (overhead, G&A, etc.) matching pool type billed, and mixed invoice interest allocates proportionally across direct and indirect components based on original invoice composition. Written procedures ensure consistent methodology application while supporting audit defense when DCAA examines crediting practices.

Create interest credit journal entries or accounting transactions implementing credits against appropriate cost objectives, with clear descriptions referencing triggering invoices, interest amounts, and crediting rationale. Detailed transaction documentation provides audit trail demonstrating compliance with crediting requirements through systematic accounting treatment rather than arbitrary or incomplete credit application.

Establish interest expense offset procedures when contractors incur interest expense requiring offset before crediting excess against cost objectives, documenting offset calculations, determining excess amounts available for cost crediting, and maintaining records supporting offset methodology and credit determinations. Offset documentation becomes particularly important when interest expense is unallowable, requiring careful documentation showing credit treatment logic.

Step 4: Integrate Interest Credits into Indirect Rate Calculations

Implement indirect pool crediting procedures ensuring Prompt Payment interest relating to indirect cost billings reduces pool costs before rate calculations, maintaining rate accuracy reflecting actual net costs after interest credit offsets. Configure rate calculation processes to incorporate interest credits systematically rather than through manual adjustments that might be overlooked or applied inconsistently.

Deploy monthly or quarterly rate calculations including current period interest credits, preventing rate distortion from delayed annual crediting and improving interim billing accuracy through rates reflecting current period interest impacts. Frequent rate calculation with current interest crediting maintains rate accuracy supporting both contractor management visibility and customer billing precision.

Develop rate reconciliation procedures verifying total indirect pool costs used for rate calculations properly reflect all applicable interest credits, with validation that credited amounts match identified interest receipts for relevant pools. Reconciliation provides assurance that interest crediting occurred completely and accurately rather than assuming processes functioned properly without verification.

Step 5: Maintain Comprehensive Interest Documentation for Audit Support

Create organized interest accounting files consolidating: interest receipt documentation showing amounts and payment details, invoice-interest matching analysis supporting cost objective identification, interest crediting calculations and journal entries, indirect rate impact analysis when applicable, and methodological documentation explaining crediting approaches for complex situations. Comprehensive files enable efficient audit response while demonstrating systematic compliance with cost crediting requirements.

Prepare annual interest summary schedules showing: total interest income received, amounts credited to specific contracts with contract identifications, amounts credited to indirect pools by pool type, any amounts offset against interest expense with supporting calculations, and reconciliation to general ledger interest accounts. Summary schedules provide efficient overview enabling management review and audit verification without requiring detailed transaction examination.

Implement pre-submission review procedures before incurred cost proposal preparation, validating that all Prompt Payment interest received during fiscal year was properly credited to contracts or indirect pools, that indirect rate calculations reflect interest credits, and that documentation supports crediting methodology. Pre-submission review catches crediting errors enabling correction before official submission rather than discovering problems during DCAA audits.

The Investment in Prompt Payment Interest Compliance

Implementing comprehensive Prompt Payment interest accounting costs between $5,000 and $15,000 for small to mid-sized contractors including procedure development, system configuration, tracking implementation, and training. Annual maintenance costs typically run $2,000 to $6,000 for ongoing interest tracking, crediting processing, and compliance monitoring. These modest investments prevent questioned costs potentially exceeding annual interest receipts through proper cost crediting compliance.

Let me show you the value: contractors with proper interest accounting credit Prompt Payment receipts against costs as regulations require, avoiding questioned costs from improper income treatment during incurred cost audits. They maintain accurate indirect rates reflecting interest credits preventing rate overstatement affecting all contracts using those rates. They demonstrate cost accounting discipline through systematic crediting supporting efficient audit processes.

Contractors with inadequate interest accounting face questioned costs equal to all improperly treated interest when DCAA discovers receipts classified as income rather than cost credits, experience indirect rate adjustments requiring billing corrections when pool costs were overstated by uncredited interest, and waste accounting staff time reconstructing crediting during audits rather than implementing proper procedures enabling routine processing.

Understanding Prompt Payment Interest Requirements Across Contract Types

Prompt Payment Act protections apply uniformly across all federal contracts regardless of agency or contract type, with automatic interest accruing on late payments for cost-reimbursement, fixed-price, time-and-materials, and other contract structures. However, cost accounting treatment requirements for interest receipts affect primarily cost-reimbursement contracts where cost crediting directly reduces government reimbursement, though indirect rate impacts extend to all contract types using those rates.

The Act applies consistently across Department of Defense, NASA, Department of Energy, and civilian agencies, with payment timelines and interest calculation methodologies uniform across federal government preventing agency-specific variations. Your interest accounting procedures should satisfy requirements across all agencies through comprehensive approach serving entire contract portfolio.

Your Path to Prompt Payment Interest Compliance

The Prompt Payment interest landscape rewards contractors who implement systematic tracking, proper crediting, and comprehensive documentation rather than treating interest as incidental income requiring no special accounting attention. DCAA evaluates interest treatment through incurred cost audit review examining whether receipts properly credited against costs as FAR requires.

For contractors seeking interest accounting compliance, Hour Timesheet provides labor tracking supporting documentation of accounting staff time spent on interest processing, demonstrating organizational investment in proper cost treatment and enabling time-based cost analysis of compliance activities.

Your Prompt Payment interest receipts deserve systematic accounting ensuring proper cost crediting, accurate rate calculations, and audit verification. Implement procedures transforming interest from accounting afterthought into systematically managed cost accounting element.