MMAS Compliance: The 10 Standards Every Government Contractor Must Know

If your material accounting system can’t pass scrutiny, neither can your contract.

I’ve sat across the table from contractors who genuinely believed their inventory tracking was adequate — right up until the moment a DCAA auditor flagged a $400,000 cost disallowance for unsupported material charges. The system wasn’t fraudulent. It was just incomplete. And in federal contracting, incomplete is expensive.

Material Management and Accounting Systems (MMAS) don’t get the attention that labor timekeeping does, but they should. For contractors who purchase, store, and consume direct materials on government contracts, a non-compliant MMAS is one of the fastest paths to a Contractor Business System Deficiency — and everything that comes with it.

Let me walk you through what the regulations actually require, where contractors consistently fall short, and how to fix it before it costs you.

The Legal Foundation You Can’t Ignore

MMAS compliance is not optional guidance — it’s a contractual obligation backed by federal regulation.

The primary authority is DFARS 252.242-7004, which establishes the ten mandatory standards for contractor material management and accounting systems. If you hold a covered contract with the Department of Defense, this clause is likely already in your agreement. The companion regulation, DFARS 242.7201–242.7203, defines the government’s audit rights and the consequences of a significant deficiency finding.

Supporting this framework, FAR 31.201-4 requires that costs be adequately documented and allocated in a manner consistent with the contractor’s disclosed accounting practices. When material charges hit a contract without a traceable audit trail back to an approved MMAS, that cost can be disallowed outright — regardless of whether the material was actually used on the job.

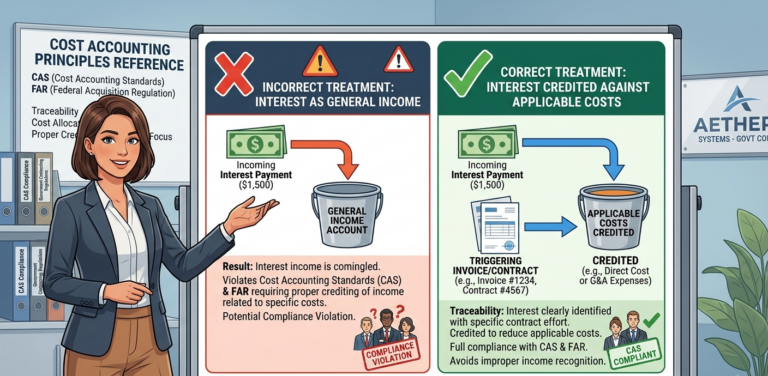

For contractors subject to Cost Accounting Standards, CAS 407 adds another layer: standard costs used in estimating, accumulating, and reporting must be consistent. If your MMAS uses standard costs that deviate significantly from actual costs without proper variance analysis and disclosure, you have a CAS compliance issue sitting inside your material system.

These aren’t abstract references. They are the exact citations DCAA auditors pull when they write up a business system deficiency. If you want to understand the full audit framework, the DCAA Contract Audit Manual (CAM), Chapter 5 is publicly available and worth bookmarking.

The 10 MMAS Standards — And Where Contractors Miss Them

DFARS 252.242-7004 lays out ten specific standards your system must meet. Here’s what they require and, more importantly, where audits go sideways:

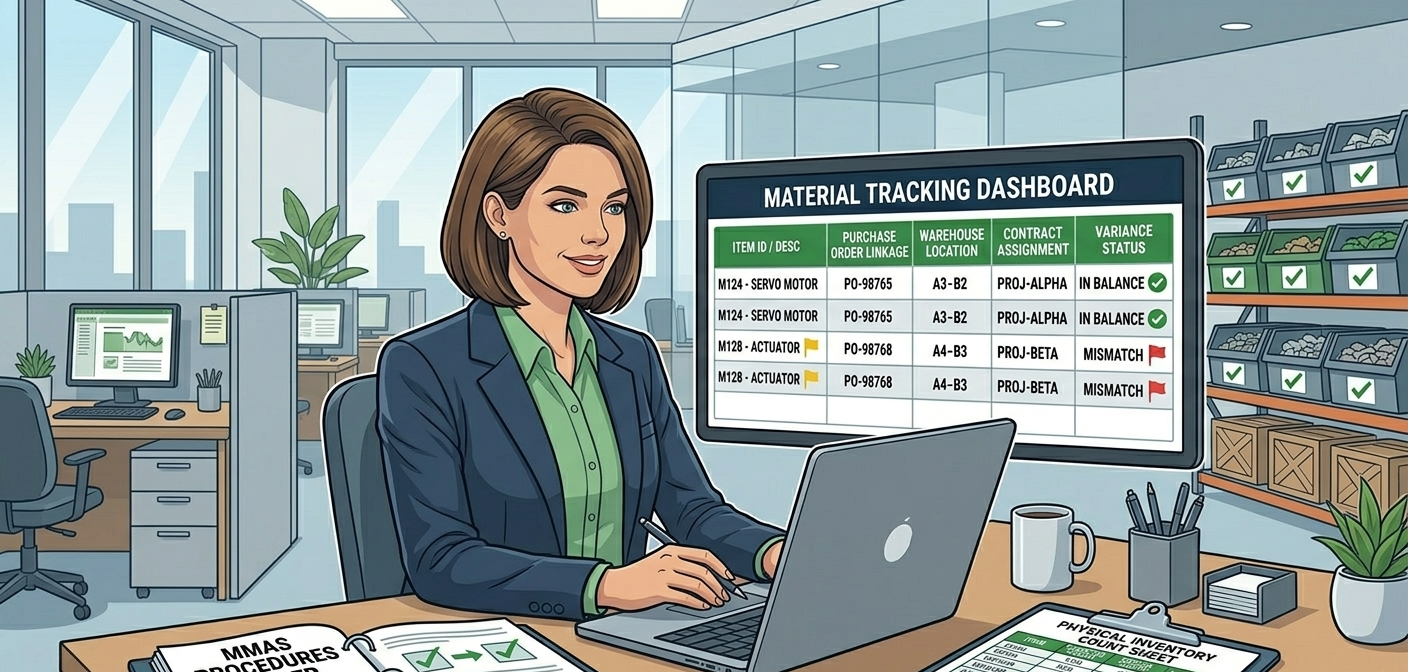

1. Proper identification of all purchased and fabricated parts. Every part must be uniquely identified in a way that ties to your contract structure. The common failure: part numbers that exist in a procurement system but don’t flow into cost accounting.

2. Accurate valuation of materials. Whether you use actual cost, standard cost, or moving average, the method must be consistently applied and disclosed. Switching methods mid-contract without disclosure is an immediate red flag.

3. Proper segregation of preproduction costs. Engineering and prototype materials must be coded separately from production runs. Commingling these is one of the most frequent findings I’ve seen on cost-plus contracts.

4. A system that identifies and reports scrap and spoilage. If your warehouse staff are throwing away defective material without a documented scrap transaction, those costs are floating — and the government will want to know where they landed.

5. Periodic physical inventories. Cycle counts are not optional. The frequency must be documented in your written procedures, and variances must be investigated and recorded. “We do counts when things seem off” does not satisfy this standard.

6. Reconciliation of physical inventory to recorded amounts. Counts alone aren’t enough — you have to reconcile discrepancies and document the resolution. A spreadsheet with unexplained adjustments is an audit finding waiting to happen.

7. Adequate controls to prevent unauthorized use or misappropriation. This includes access controls, approval workflows, and documented issuance procedures. Here’s what contractors miss: this isn’t just a physical security question. It includes controls over who can post transactions in your ERP system.

8. Timely recording of transactions. Material should be charged to contracts when it’s issued, not when the invoice is processed or when someone has time to update the system. Lag in recording creates mismatches between physical consumption and financial reporting.

9. Applicable material management techniques (e.g., MRP). For contractors using Manufacturing Resource Planning, the system must be documented and operating as described. Using MRP in name but not in practice creates a significant exposure.

10. Written policies and procedures. This is the foundation everything else rests on. Without documented procedures that match your actual practice, you have no defense when an auditor challenges a transaction.

Five Steps to Build a Compliant MMAS

Step 1: Document your system in writing — completely. Your written MMAS procedures must describe every process listed in DFARS 252.242-7004. If an auditor asks how you value inventory and your answer isn’t in writing, the system fails on that standard alone.

Step 2: Map your material flow from PO to contract charge. Walk a single purchase order through your system end-to-end. Can you trace it from the vendor invoice to the warehouse receipt, to the job issuance, to the contract cost? If the chain breaks anywhere, fix it before an auditor finds it.

Step 3: Establish and document cycle count procedures. Set a documented frequency — quarterly for high-value items, annually at minimum for all parts. Record your counts, document variances over a defined threshold, and sign off on resolutions. This creates the audit trail the standard requires.

Step 4: Align your ERP configuration with your written procedures. Your system should enforce the controls you’ve described on paper. If your written procedure says material requires a supervisor approval for issuance, your ERP should require that approval before the transaction posts. Gaps between policy and system configuration are where deficiency findings are born.

Step 5: Conduct an internal pre-audit review annually. Before DCAA shows up, you should have already tested your system against the ten standards. Document the review, note any gaps, and show remediation. Auditors respond well to contractors who identify and fix their own issues — it demonstrates a culture of compliance.

For more on building defensible internal controls, see our related posts on DCAA timekeeping compliance and cost accounting system requirements.

The Real Cost Comparison

A formal MMAS assessment from an outside consultant typically runs $5,000–$15,000. Implementing ERP configuration changes to enforce proper controls might add another $10,000–$25,000 depending on your system.

Compare that to a significant deficiency finding: under DFARS 252.242-7004, the government can withhold 5% of progress payments or performance-based payments until the deficiency is corrected. On a $5 million contract, that’s $250,000 in withheld cash. Add the cost of a contractor response, corrective action plan, re-audit, and potential cost disallowances — and the math becomes obvious.

Compliance is an investment. Non-compliance is a tax.

Jurisdictional Note

DFARS 252.242-7004 applies to DoD contractors with covered contracts — generally those with cost-reimbursement, incentive, time-and-material, or labor-hour contracts over $2 million. However, civilian agency contracts under FAR Part 31 still require adequate material accounting documentation for cost allowability purposes. If you’re performing work across both DoD and civilian agencies, build your MMAS to the higher DFARS standard and it will satisfy both.

The ten MMAS standards exist because material costs are real money, and the government wants assurance that the money it’s paying for material actually went to the contract it’s paying for. A well-documented, consistently applied material accounting system is your best protection — and it’s not nearly as complicated to build as a deficiency finding is to survive.

Hour Timesheet helps government contractors manage compliant timekeeping and cost tracking. Learn more about our DCAA-compliant time and billing tools.

If your material accounting system can’t pass scrutiny, neither can your contract.

I’ve sat across the table from contractors who genuinely believed their inventory tracking was adequate — right up until the moment a DCAA auditor flagged a $400,000 cost disallowance for unsupported material charges. The system wasn’t fraudulent. It was just incomplete. And in federal contracting, incomplete is expensive.

Material Management and Accounting Systems (MMAS) don’t get the attention that labor timekeeping does, but they should. For contractors who purchase, store, and consume direct materials on government contracts, a non-compliant MMAS is one of the fastest paths to a Contractor Business System Deficiency — and everything that comes with it.

Let me walk you through what the regulations actually require, where contractors consistently fall short, and how to fix it before it costs you.

The Legal Foundation You Can’t Ignore

MMAS compliance is not optional guidance — it’s a contractual obligation backed by federal regulation.

The primary authority is DFARS 252.242-7004, which establishes the ten mandatory standards for contractor material management and accounting systems. If you hold a covered contract with the Department of Defense, this clause is likely already in your agreement. The companion regulation, DFARS 242.7201–242.7203, defines the government’s audit rights and the consequences of a significant deficiency finding.

Supporting this framework, FAR 31.201-4 requires that costs be adequately documented and allocated in a manner consistent with the contractor’s disclosed accounting practices. When material charges hit a contract without a traceable audit trail back to an approved MMAS, that cost can be disallowed outright — regardless of whether the material was actually used on the job.

For contractors subject to Cost Accounting Standards, CAS 407 adds another layer: standard costs used in estimating, accumulating, and reporting must be consistent. If your MMAS uses standard costs that deviate significantly from actual costs without proper variance analysis and disclosure, you have a CAS compliance issue sitting inside your material system.

These aren’t abstract references. They are the exact citations DCAA auditors pull when they write up a business system deficiency. If you want to understand the full audit framework, the DCAA Contract Audit Manual (CAM), Chapter 5 is publicly available and worth bookmarking.

The 10 MMAS Standards — And Where Contractors Miss Them

DFARS 252.242-7004 lays out ten specific standards your system must meet. Here’s what they require and, more importantly, where audits go sideways:

1. Proper identification of all purchased and fabricated parts. Every part must be uniquely identified in a way that ties to your contract structure. The common failure: part numbers that exist in a procurement system but don’t flow into cost accounting.

2. Accurate valuation of materials. Whether you use actual cost, standard cost, or moving average, the method must be consistently applied and disclosed. Switching methods mid-contract without disclosure is an immediate red flag.

3. Proper segregation of preproduction costs. Engineering and prototype materials must be coded separately from production runs. Commingling these is one of the most frequent findings I’ve seen on cost-plus contracts.

4. A system that identifies and reports scrap and spoilage. If your warehouse staff are throwing away defective material without a documented scrap transaction, those costs are floating — and the government will want to know where they landed.

5. Periodic physical inventories. Cycle counts are not optional. The frequency must be documented in your written procedures, and variances must be investigated and recorded. “We do counts when things seem off” does not satisfy this standard.

6. Reconciliation of physical inventory to recorded amounts. Counts alone aren’t enough — you have to reconcile discrepancies and document the resolution. A spreadsheet with unexplained adjustments is an audit finding waiting to happen.

7. Adequate controls to prevent unauthorized use or misappropriation. This includes access controls, approval workflows, and documented issuance procedures. Here’s what contractors miss: this isn’t just a physical security question. It includes controls over who can post transactions in your ERP system.

8. Timely recording of transactions. Material should be charged to contracts when it’s issued, not when the invoice is processed or when someone has time to update the system. Lag in recording creates mismatches between physical consumption and financial reporting.

9. Applicable material management techniques (e.g., MRP). For contractors using Manufacturing Resource Planning, the system must be documented and operating as described. Using MRP in name but not in practice creates a significant exposure.

10. Written policies and procedures. This is the foundation everything else rests on. Without documented procedures that match your actual practice, you have no defense when an auditor challenges a transaction.

Five Steps to Build a Compliant MMAS

Step 1: Document your system in writing — completely. Your written MMAS procedures must describe every process listed in DFARS 252.242-7004. If an auditor asks how you value inventory and your answer isn’t in writing, the system fails on that standard alone.

Step 2: Map your material flow from PO to contract charge. Walk a single purchase order through your system end-to-end. Can you trace it from the vendor invoice to the warehouse receipt, to the job issuance, to the contract cost? If the chain breaks anywhere, fix it before an auditor finds it.

Step 3: Establish and document cycle count procedures. Set a documented frequency — quarterly for high-value items, annually at minimum for all parts. Record your counts, document variances over a defined threshold, and sign off on resolutions. This creates the audit trail the standard requires.

Step 4: Align your ERP configuration with your written procedures. Your system should enforce the controls you’ve described on paper. If your written procedure says material requires a supervisor approval for issuance, your ERP should require that approval before the transaction posts. Gaps between policy and system configuration are where deficiency findings are born.

Step 5: Conduct an internal pre-audit review annually. Before DCAA shows up, you should have already tested your system against the ten standards. Document the review, note any gaps, and show remediation. Auditors respond well to contractors who identify and fix their own issues — it demonstrates a culture of compliance.

For more on building defensible internal controls, see our related posts on DCAA timekeeping compliance and cost accounting system requirements.

The Real Cost Comparison

A formal MMAS assessment from an outside consultant typically runs $5,000–$15,000. Implementing ERP configuration changes to enforce proper controls might add another $10,000–$25,000 depending on your system.

Compare that to a significant deficiency finding: under DFARS 252.242-7004, the government can withhold 5% of progress payments or performance-based payments until the deficiency is corrected. On a $5 million contract, that’s $250,000 in withheld cash. Add the cost of a contractor response, corrective action plan, re-audit, and potential cost disallowances — and the math becomes obvious.

Compliance is an investment. Non-compliance is a tax.

Jurisdictional Note

DFARS 252.242-7004 applies to DoD contractors with covered contracts — generally those with cost-reimbursement, incentive, time-and-material, or labor-hour contracts over $2 million. However, civilian agency contracts under FAR Part 31 still require adequate material accounting documentation for cost allowability purposes. If you’re performing work across both DoD and civilian agencies, build your MMAS to the higher DFARS standard and it will satisfy both.

The ten MMAS standards exist because material costs are real money, and the government wants assurance that the money it’s paying for material actually went to the contract it’s paying for. A well-documented, consistently applied material accounting system is your best protection — and it’s not nearly as complicated to build as a deficiency finding is to survive.

Hour Timesheet helps government contractors manage compliant timekeeping and cost tracking. Learn more about our DCAA-compliant time and billing tools.