Cost Estimating System Requirements: Accuracy in Bid Development

A proposal isn’t just a sales document. In federal contracting, it’s a legal representation of your costs — and DCAA treats it that way.

I’ve watched contractors win contracts and then spend the next twelve months trying to reconcile what they bid against what they’re actually spending. Sometimes the gap is explainable. Sometimes it’s not. When it’s not — when the estimating methodology was inconsistent, the historical data was selectively applied, or the basis of estimate was assembled under deadline pressure without a documented process behind it — that’s when a routine incurred cost audit turns into a defective pricing investigation.

The cost estimating system doesn’t get the attention it deserves at small contracting firms. Most of the focus goes to timekeeping and billing, which are important, but your exposure often starts earlier — at the proposal stage, before the contract is even signed. If your estimating system can’t demonstrate a consistent, documented, and auditable methodology, you’re building compliance risk into every contract from day one.

Let me show you what the regulations require, where the common gaps are, and how to build a system that holds up.

The Legal Foundation

The requirements for an adequate cost estimating system are rooted in several overlapping regulatory frameworks that apply from the moment you begin developing a bid.

DFARS 252.215-7002 establishes the specific standards for contractor cost estimating systems on covered DoD contracts. It requires that your system produce proposals that are consistent with your disclosed cost accounting practices, supported by appropriate historical data, and traceable from the summary level down to the underlying cost basis. This clause also gives DCAA the authority to review and formally assess your estimating system — and to issue a significant deficiency finding if it doesn’t measure up.

FAR 15.408, Table 15-2 defines the format and content requirements for cost or pricing data submissions on negotiated contracts above the Truth in Negotiations Act threshold — currently set under 41 U.S.C. 1702. When your contract requires certified cost or pricing data, every element of your proposal must be accurate, complete, and current as of the date of agreement on price. An estimating system that can’t produce proposals meeting those standards creates defective pricing exposure — which carries the right of the government to a price reduction equal to the amount of any overstated costs, plus interest.

For CAS-covered contractors, CAS 401 requires that the cost accounting practices used in estimating be consistent with the practices used in accumulating and reporting actual costs. If you estimate labor using one set of assumptions and then charge labor using a different methodology, you have a CAS noncompliance issue embedded in your estimating process.

The DCAA Contract Audit Manual, Chapter 9 lays out the full framework for estimating system audits, including the specific attributes auditors examine. It is the most useful single reference a contractor can read before preparing for an estimating system review.

What an Adequate Estimating System Actually Requires

Here’s what contractors miss: the adequacy standards for a cost estimating system aren’t about whether your bids are accurate. They’re about whether your process for developing bids is systematic, documented, and consistent. DCAA is evaluating the system — not just the output.

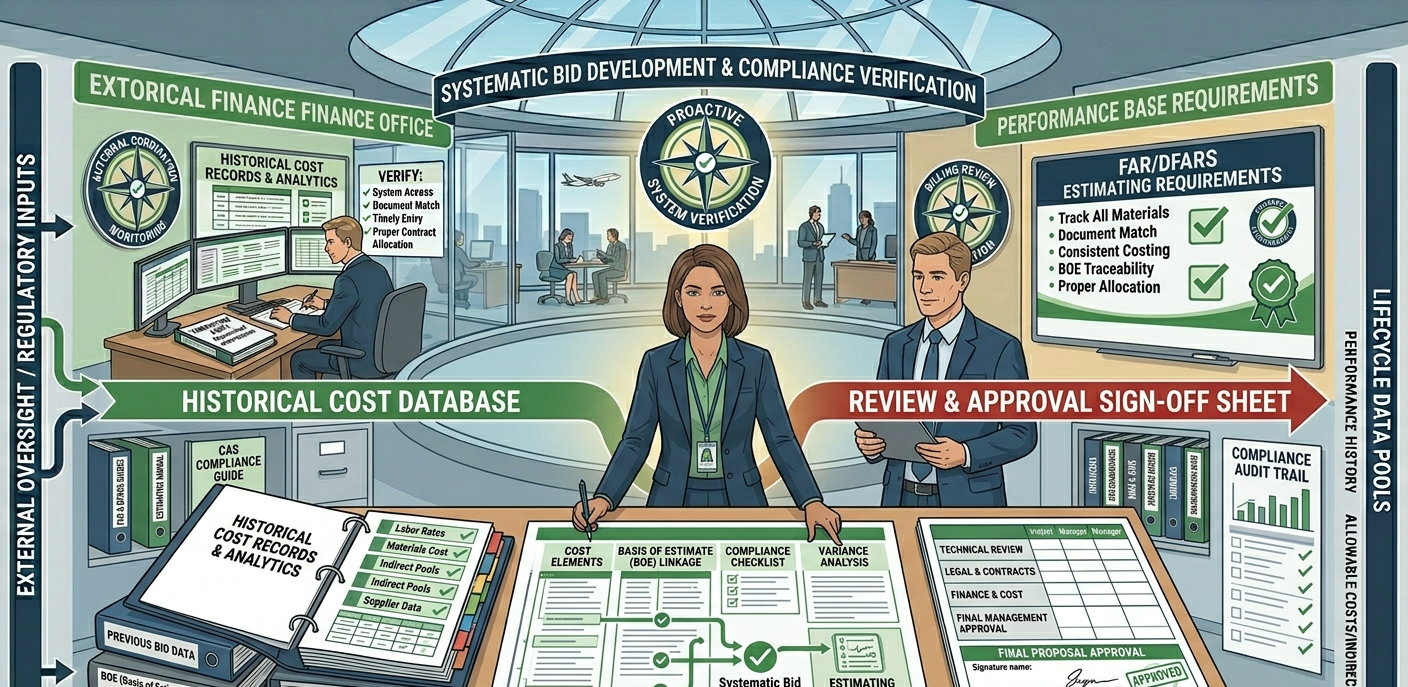

Under DFARS 252.215-7002, an adequate system must demonstrate several core capabilities. It must establish clear responsibility for the preparation, review, and approval of each cost estimate. It must use appropriate historical data from your own cost experience — not just industry benchmarks or rough analogies. It must apply those historical rates and factors consistently across proposals. It must produce estimates that reconcile to your accounting system’s cost structure. And it must maintain documentation sufficient to allow an auditor to trace every line item in a proposal back to its basis.

This is where audits go sideways. The estimating system looks fine from the outside — the proposals are formatted correctly, the numbers are reasonable, the indirect rates are properly applied. But when an auditor asks to see the basis of estimate for a specific labor category, the answer is a spreadsheet that one person built from memory and a previous proposal that may or may not be applicable. There’s no documented methodology, no connection to actual cost history, and no review trail. That’s a system deficiency — regardless of whether the final price was fair.

The second common gap is the disconnect between estimating and accounting. A contractor builds a proposal using labor categories and cost elements that make sense for the bid — and then charges the contract using a completely different cost structure because that’s how the accounting system is set up. When DCAA reconciles the proposal to the actual costs, the mapping doesn’t work. That creates questions that are difficult to answer without a documented bridge between the two systems.

The third gap is the treatment of subcontractor costs. Prime contractors are responsible for the adequacy of their subcontractor cost or pricing data when it flows into a certified submission. Accepting a subcontractor quote without adequate documentation and analysis — and then incorporating it into a proposal as if it were fully supported — is a defective pricing exposure that sits at the prime level, not the subcontractor level.

Five Steps to Build a Compliant Estimating System

Step 1: Document your estimating methodology in writing. Every cost element in your standard proposal — direct labor, materials, subcontracts, ODCs, indirect rates — should have a written methodology describing how it’s estimated, what data sources are used, and who is responsible for its development and review. This document is the foundation of your estimating system. Without it, every proposal is an ad hoc exercise rather than a systematic process.

Step 2: Build your estimates from your own historical cost data. The most defensible basis of estimate is your own actual cost experience. Maintain a structured historical database — labor hours by labor category and contract type, material costs by commodity, subcontract performance data — and reference it explicitly in every estimate. When you deviate from historical experience, document why. Auditors are not troubled by variances; they are troubled by variances without explanations.

Step 3: Align your proposal cost structure with your accounting system. Your proposal labor categories, indirect cost pools, and cost element structure should mirror your accounting system’s structure. If your accounting system accumulates costs by direct labor, fringe, overhead, G&A, and fee — your proposals should be built in the same framework. A DCAA-compliant cost accounting system that feeds historical actuals directly into your estimating process is the most efficient way to maintain this alignment.

Step 4: Establish a formal proposal review and approval process. Every proposal above a defined threshold should go through a documented review — technical lead confirms hours, finance confirms rates, management approves before submission. The review should be evidenced: a sign-off sheet, an email approval chain, a review checklist. When DCAA asks who reviewed the proposal and what they checked, you should be able to answer both questions with documentation in hand.

Step 5: Conduct a post-award estimate-to-actual analysis on completed contracts. After each contract closes, compare your original estimate to your actual costs by cost element. Document significant variances and use them to improve your estimating methodology. This feedback loop is what transforms an estimating system from a compliance exercise into a genuine management tool — and it’s exactly what DCAA wants to see as evidence that your system is self-correcting. For guidance on structuring your cost accounting to support this kind of analysis, see our post on incurred cost submission preparation.

The Cost of Getting It Wrong

A defective pricing finding under the Truth in Negotiations Act entitles the government to a price reduction equal to the amount of overstated costs — plus interest from the date of contract award. On a contract priced at several million dollars, a relatively modest overstatement can produce a six-figure repayment obligation.

An estimating system deficiency finding under DFARS 252.215-7002 can trigger withholding of up to five percent of contract billings across all affected contracts until the deficiency is corrected. For a contractor with multiple active cost-reimbursement contracts, that withholding can represent a significant cash flow impact sustained over months.

Contrast that with the cost of building a compliant estimating system: documented methodologies, a structured historical database, a proposal review process, and an accounting system alignment review. For most small contractors, that investment runs between $15,000 and $40,000 depending on existing systems and the complexity of the contract portfolio. It is, without exception, less expensive than the first significant finding.

Jurisdictional Notes

DFARS 252.215-7002 applies specifically to DoD contracts meeting the coverage thresholds — generally cost-reimbursement and incentive contracts above established dollar levels. However, the Truth in Negotiations Act requirements under FAR 15.408 apply to all federal agencies on negotiated contracts above the certified cost or pricing data threshold. Civilian agency contractors are not subject to DFARS estimating system oversight but remain exposed to defective pricing claims under FAR. Contractors performing across both DoD and civilian agencies should build their estimating system to the DFARS standard — it satisfies both frameworks.

The proposal is where your compliance posture either starts strong or starts compromised. A well-documented, consistently applied cost estimating system isn’t just an audit requirement — it’s the foundation of every contract you’ll ever win. Build it right, maintain it actively, and it becomes one of your firm’s most durable competitive advantages.

Hour Timesheet gives government contractors the timekeeping and cost tracking infrastructure that feeds accurate historical data into every proposal you build. See how our platform supports your estimating and compliance program.