Progress Payments vs. Performance-Based Payments: DCAA Logic

Most contractors understand that the government pays them. Fewer understand that how the government pays them determines how DCAA audits them — and those are very different things.

I’ve seen small contractors walk into a contract financing arrangement without fully understanding which payment mechanism they agreed to. By the time they realize the difference, they’re already sitting across from a DCAA auditor who’s asking for cost records they didn’t know they needed to keep in a specific format. The contract was performing fine. The billing was on time. But the documentation behind the payment requests didn’t match the financing type — and that created a finding that took months to resolve.

Contract financing is where a lot of compliance exposure lives for growing contractors. Understanding the difference between progress payments and performance-based payments isn’t just a finance question. It’s a compliance question, and DCAA treats the two very differently.

Let me walk you through the logic.

The Legal Foundation

The two primary contract financing mechanisms for federal contractors are governed by distinct regulatory frameworks, and they carry different audit obligations.

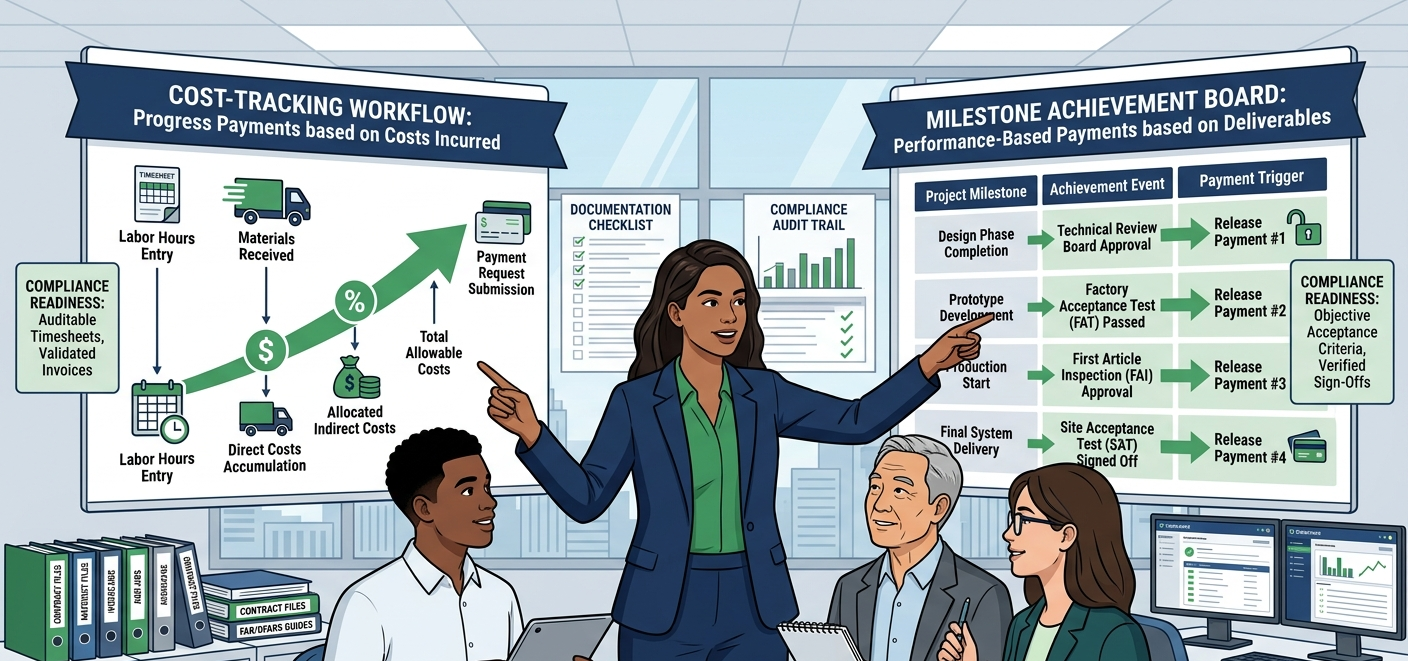

FAR 32.5 governs traditional progress payments, which are financing payments based on costs incurred. The government advances funds as the contractor spends money — on labor, materials, and overhead — in anticipation of final delivery. Because these payments are tied directly to incurred costs, DCAA has full audit authority over the cost records that support every payment request. The contractor must be able to demonstrate that the costs claimed are allocable, allowable, and properly documented under FAR 31.201-2.

FAR 32.10 governs performance-based payments, which are structured around the achievement of defined contract events or milestones rather than costs incurred. The government pays when work is accomplished, not when money is spent. This is an important distinction: performance-based payments are not an advance against costs — they are financing tied to objective, measurable outcomes defined in the contract.

Underlying both mechanisms is 10 U.S.C. 3801 (formerly 10 U.S.C. 2307), which authorizes the use of contract financing for defense acquisitions and establishes the government’s security interest in contractor assets when progress payments are in use. That security interest has real teeth — when you accept progress payments, the government holds a lien on your work in process and finished goods until delivery and final payment. That’s not a detail to overlook.

The DCAA Contract Audit Manual, Chapter 6 covers the audit procedures for both financing types in detail and is worth reviewing before your first payment request goes out the door.

How the Two Mechanisms Actually Work

Understanding the structural difference between these two payment types is the foundation of compliance. Here’s what contractors miss when they treat them interchangeably.

Progress payments are calculated as a percentage of total costs incurred — typically up to 80% for large businesses and 85% for small businesses under FAR 52.232-16. You submit a progress payment request showing your cumulative costs to date, and the government advances a corresponding percentage of those costs. The audit obligation is continuous: DCAA can review your cost accumulation system, your labor charging practices, your material accounting, and your billing at any point during contract performance. Your DCAA-compliant accounting system is not just a best practice under progress payments — it is a contractual prerequisite.

Performance-based payments work differently. The contracting officer and contractor agree in advance on a set of performance events — completion of a design review, delivery of a prototype, passage of a specific test — and assign a payment value to each event. When the contractor demonstrates completion of the event, the payment is triggered. Cost records are not the basis for the payment request. The event completion is.

This is where audits go sideways: contractors operating under performance-based payments sometimes assume they have reduced audit exposure because DCAA isn’t reviewing costs on a rolling basis. That assumption is wrong. While the payment trigger is event-based, the contractor’s underlying accounting system must still comply with FAR 31.2 cost principles for any cost-reimbursable elements of the contract, and DCAA retains the right to conduct post-award audits of incurred costs. The payment mechanism changes the billing structure — it does not change the compliance obligations.

What Contractors Get Wrong

The most common mistake is a documentation mismatch. Contractors on progress payments submit payment requests that reference costs incurred but can’t produce a clean audit trail from those costs back to their accounting system. The cost appears on the request but isn’t traceable to a specific job, cost element, or time period in the underlying records.

The second mistake is treating performance-based payment milestones as informal. The event criteria must be objective and measurable, and completion must be documented at the time it occurs — not reconstructed after the fact when a payment request is pending. An auditor reviewing a milestone completion with no contemporaneous evidence is going to question whether the event was genuinely complete at the time of billing.

The third mistake is failing to maintain the government’s security interest documentation under progress payments. When the government holds a lien on your work in process, you need to be able to account for that inventory separately from commercial work if you have mixed contracts. Commingling government and commercial work in process is a compliance gap that shows up on business system reviews.

Five Steps to Stay Compliant Under Either Mechanism

Step 1: Know which financing type is in your contract and read the clause. FAR 52.232-16 governs progress payments. FAR 52.232-32 governs performance-based payments. Pull the clause from your contract and read it before your first payment request. The documentation requirements are spelled out explicitly — follow them exactly.

Step 2: Build your payment request documentation package before you need it. For progress payments, that means a cost summary tied to your accounting system by cost element and period. For performance-based payments, that means contemporaneous evidence of milestone completion — sign-off sheets, test results, deliverable receipts — organized and ready to produce at the time of billing.

Step 3: Maintain a clean audit trail from payment request to accounting records. Every dollar on a progress payment request must trace directly to your job cost ledger. Run a reconciliation before submission, not after DCAA asks for one. A DCAA-compliant timekeeping and cost tracking system makes this reconciliation routine rather than reactive.

Step 4: Document milestone completions at the time they occur. For performance-based payments, create a standard completion package for each milestone — a brief summary of what was accomplished, supporting evidence, and a date-stamped sign-off from a responsible manager. File it immediately. Reconstructed documentation is a red flag in any audit.

Step 5: Understand and account for the government’s lien under progress payments. Work with your accounting team to ensure that government-financed work in process is clearly identified and segregated in your inventory records. Review FAR 52.232-16(f) for the specific property requirements — and make sure your system reflects them.

The Cost of Getting It Wrong

A progress payment suspension — triggered when DCAA determines that your accounting system is inadequate to support the payment requests you’ve submitted — can halt all financing under the contract until the deficiency is corrected. For a contractor carrying significant work in process on a long-term contract, that cash flow interruption can be operationally devastating. Suspension periods routinely run 60 to 180 days while corrective action plans are negotiated and re-audited.

The cost of building a compliant accounting system and documentation process up front — proper job costing, clean labor distribution, organized milestone documentation — typically runs $10,000 to $30,000 for a small contractor implementing or upgrading their systems. That’s a fraction of the carrying cost of a 90-day payment suspension on a contract of any meaningful size.

Jurisdictional Notes

Progress payments under FAR 32.5 and performance-based payments under FAR 32.10 are available across both DoD and civilian agency contracts. DoD contracts are subject to additional DFARS provisions — including the business system requirements under DFARS 252.242-7006 — that govern the adequacy of the accounting system supporting payment requests. Civilian agency contracts follow FAR Part 31 cost principles but are generally not subject to DFARS business system oversight. Contractors performing across both agency types should build to the higher DoD standard.

The choice between progress payments and performance-based payments is a contracting decision. Managing the compliance obligations that come with either one is a systems and documentation decision. Get both right from the start, and financing becomes a reliable tool. Let either one drift, and it becomes a liability.

Hour Timesheet provides DCAA-compliant timekeeping and cost tracking tools built for government contractors managing complex contract financing requirements. Learn how our platform supports your compliance program.