DCAA Compliance | DCAA Timekeeping | Leave Management Software | Location Tracking | QuickBooks Desktop

DCAA Audit Preparation for Government Contractors

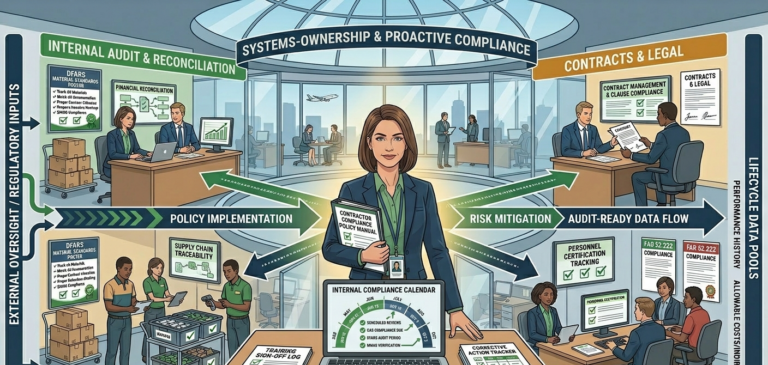

DCAA audit preparation starts long before an auditor requests records. For government contractors, labor is often one of the most closely reviewed cost areas, which makes accurate timekeeping, clear charge codes, documented approvals, and organized records essential to audit readiness. Under FAR 31.201-2, contractors are responsible for maintaining records that show claimed costs were incurred,…