DCAA Compliance | DCAA Timekeeping | Leave Management Software | Payroll | QuickBooks | Timekeeping Software

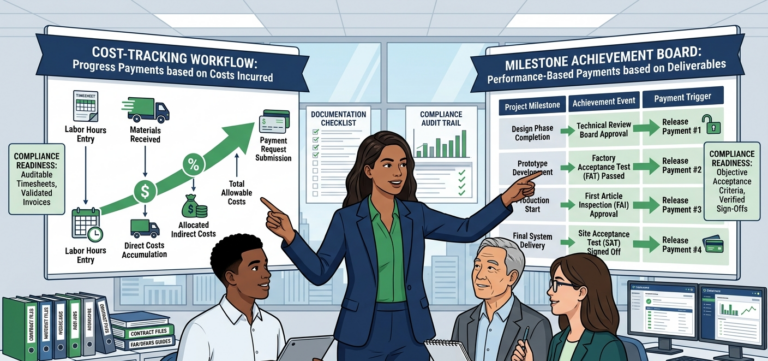

Progress Payments vs. Performance-Based Payments: DCAA Logic

Most contractors understand that the government pays them. Fewer understand that how the government pays them determines how DCAA audits them — and those are very different things. I’ve seen small contractors walk into a contract financing arrangement without fully understanding which payment mechanism they agreed to. By the time they realize the difference, they’re…