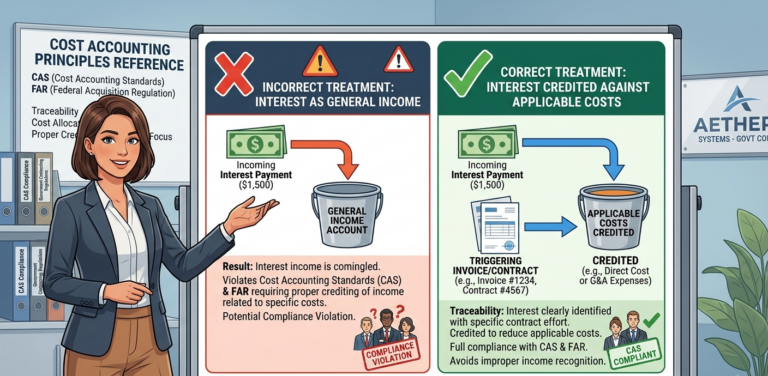

Interest Penalties under the Prompt Payment Act: GovCon Guidelines

Your company submitted a proper invoice on June 15 for completed contract deliverables, but the government didn’t process payment until September 3—79 days later—triggering automatic interest penalties of $8,400 under the Prompt Payment Act that the government paid you without dispute. Six months later during your incurred cost audit, DCAA questioned whether you properly accounted…