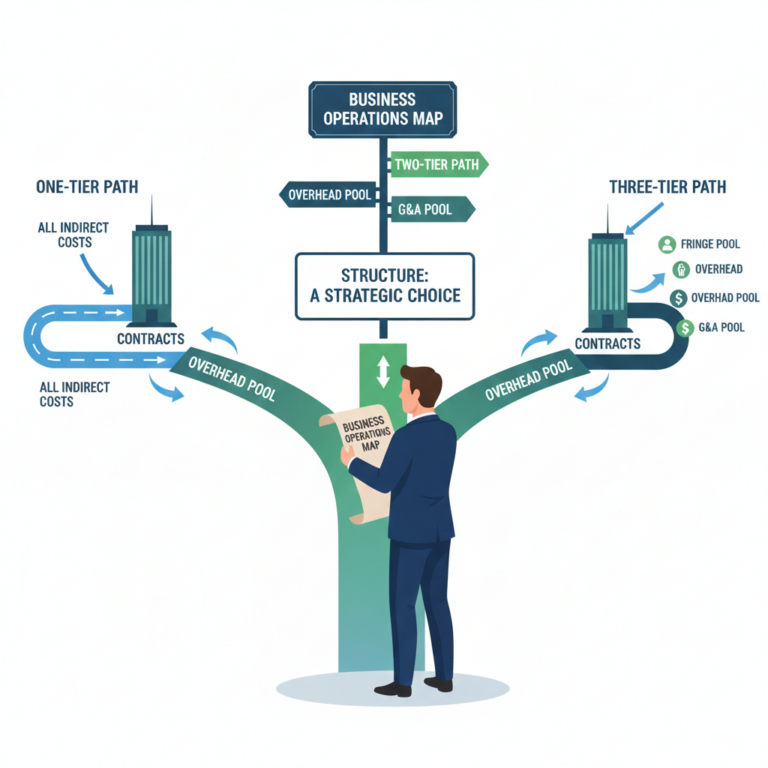

Indirect Rate Structure Design: One, Two, or Three-Tier Pools

Your company operated with a single overhead rate pooling all indirect costs—engineering support, facilities, administrative staff, and executive management—and allocating them to contracts using total direct labor as the base. During your DCAA audit, investigators discovered that your manufacturing operations consumed substantially more facility and equipment resources than your professional services work, yet both received…