DCAA Compliance | DCAA Timekeeping | Job Costing | Leave Management Software | Location Tracking | QuickBooks Desktop | QuickBooks Online

Teaming Agreement Risks: Avoiding Affiliation Issues in DCAA Audits

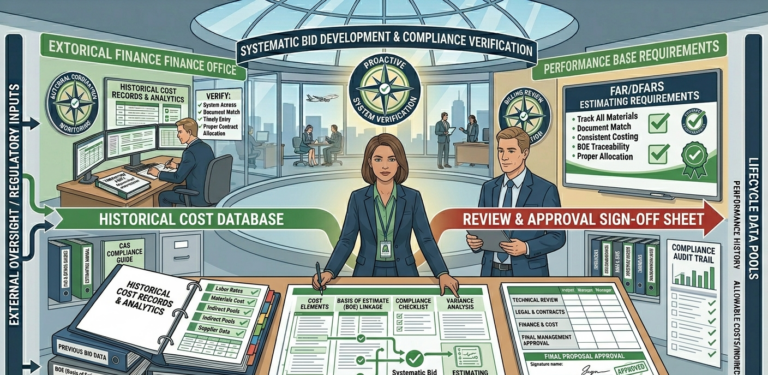

A teaming agreement that wins you a contract can also be the document that costs you your small business status — if it’s not structured correctly. I’ve seen it happen to contractors who did everything else right. They had compliant timekeeping, a clean accounting system, and a solid past performance record. They teamed with a…