DCAA Compliance | DCAA Timekeeping | Job Costing | Location Tracking | Payroll | QuickBooks | QuickBooks Desktop | QuickBooks Online | QuickBooks timesheet | Timekeeping Software

CPSR Readiness: Designing a Compliant Contractor Purchasing System

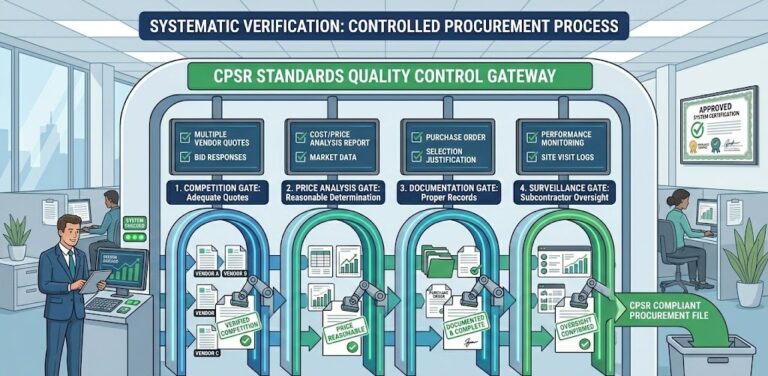

Your company won a $15 million cost-reimbursement prime contract requiring you to manage $8 million in subcontracts, triggering a mandatory Contractor Purchasing System Review (CPSR). DCMA reviewers discovered you lacked documented purchasing procedures, competitive source selection processes, price reasonableness determinations, or subcontractor risk assessments—resulting in significant deficiency findings that suspended your purchasing system approval and…